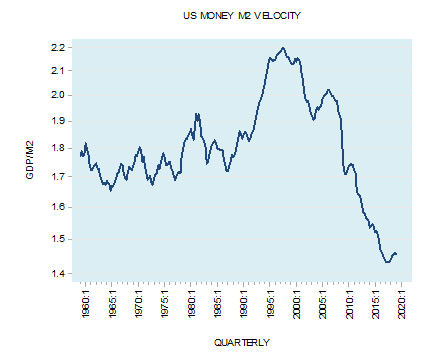

Finance velocity, in its simplest terms, is the rate at which money changes hands within an economy. It’s a crucial indicator of economic health, reflecting how quickly money is being used for transactions, investments, and overall economic activity. Think of it as a measure of how frequently a dollar is spent, saved, and re-spent within a given period, typically a year.

The basic formula for calculating the velocity of money is: V = (P x Q) / M

- V represents the velocity of money.

- P is the price level of goods and services.

- Q is the quantity of goods and services produced.

- M is the total money supply in the economy.

Therefore, the velocity of money equals the nominal GDP (P x Q) divided by the money supply. This formula helps us understand the relationship between the amount of money circulating and the overall economic output.

A high finance velocity suggests a vibrant and active economy. It means consumers and businesses are confident, spending freely, investing in projects, and generally engaging in activities that stimulate growth. Businesses are likely making sales and reinvesting profits, and individuals are comfortable making purchases rather than hoarding cash. This increased economic activity contributes to a higher GDP and overall prosperity.

Conversely, a low finance velocity often signals economic stagnation or recession. It indicates that money is circulating slowly, with consumers and businesses holding onto their funds rather than spending or investing. This could stem from uncertainty about the future, fear of job losses, or a lack of confidence in investment opportunities. When money sits idle, economic activity slows down, potentially leading to lower GDP growth, reduced employment, and deflationary pressures.

Several factors can influence finance velocity. Interest rates play a significant role. Lower interest rates tend to encourage borrowing and spending, increasing velocity. Higher rates, on the other hand, can incentivize saving and reduce spending, decreasing velocity. Consumer confidence is another key driver. Optimistic consumers are more likely to spend, boosting velocity, while pessimistic consumers tend to save more. Technological advancements can also impact velocity. The rise of online payments and digital transactions has generally accelerated the speed at which money changes hands. Inflation and deflation can also impact this number. Deflation can cause people to sit on money in hopes of a better deal later, while inflation makes people spend more quickly, thus increasing the velocity.

Central banks closely monitor finance velocity as an indicator of the effectiveness of their monetary policies. For example, if a central bank injects money into the economy through quantitative easing, it expects to see an increase in finance velocity. If velocity remains low, it may suggest that the policy isn’t effectively stimulating economic activity. However, interpreting finance velocity can be complex. Changes in velocity can be influenced by a variety of factors, and it’s not always a reliable predictor of future economic performance when used in isolation. It must be analyzed in conjunction with other economic indicators to gain a comprehensive understanding of the overall economic health and the effectiveness of monetary policy.

880×460 velocity money expertise asia from www.expertise-asia.com

880×460 velocity money expertise asia from www.expertise-asia.com  500×304 velocity money from inflationdata.com

500×304 velocity money from inflationdata.com :max_bytes(150000):strip_icc()/VelocityofM1money-1d667c2c52314c9091fd8f8696a3a0ef.JPG) 1172×505 velocity money definition from www.investopedia.com

1172×505 velocity money definition from www.investopedia.com  752×378 money velocity inflation expertise asia from www.expertise-asia.com

752×378 money velocity inflation expertise asia from www.expertise-asia.com  2560×1440 velocity money investing jay vasantharajah from jayvas.com

2560×1440 velocity money investing jay vasantharajah from jayvas.com  424×363 money velocity economic growth mises wire from mises.org

424×363 money velocity economic growth mises wire from mises.org  752×452 velocity money cls investments llc from www.clsinvest.com

752×452 velocity money cls investments llc from www.clsinvest.com  1920×1080 velocity money cpi inflation calculator updated from cpiinflationcalculator.com

1920×1080 velocity money cpi inflation calculator updated from cpiinflationcalculator.com  979×640 financial economic velocity seeking alpha from seekingalpha.com

979×640 financial economic velocity seeking alpha from seekingalpha.com  1224×599 velocity money cautionary tale sounding from thesoundingline.com

1224×599 velocity money cautionary tale sounding from thesoundingline.com