The Black-Scholes Model: A Primer

The Black-Scholes (or Black-Scholes-Merton) model is a cornerstone of modern financial theory, providing a theoretical estimate of the price of European-style options. Developed in 1973 by Fischer Black and Myron Scholes (with Robert Merton later expanding on it), it offers a mathematical formula for calculating the fair price of an option based on certain assumptions.

Key Inputs and Assumptions

The Black-Scholes model utilizes several key inputs to arrive at its theoretical option price:

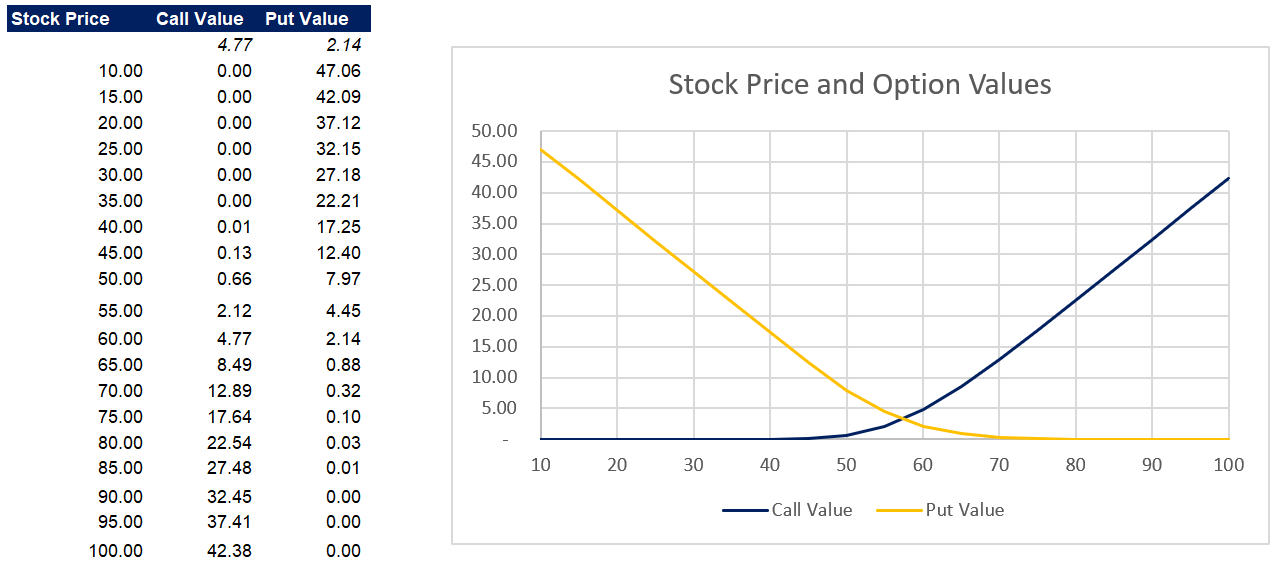

- Current Stock Price (S): The market price of the underlying asset.

- Strike Price (K): The price at which the option holder can buy (call option) or sell (put option) the underlying asset.

- Time to Expiration (T): The remaining time until the option expires, expressed in years.

- Risk-Free Interest Rate (r): The rate of return on a risk-free investment, typically the yield on a government bond with a maturity matching the option’s expiration.

- Volatility (σ): A measure of how much the underlying asset’s price is expected to fluctuate over the option’s life. This is usually expressed as the annualized standard deviation of the asset’s returns.

The model rests on several important assumptions, which are often debated in real-world applications:

- European-Style Options: The option can only be exercised at expiration.

- No Dividends: The underlying asset pays no dividends during the option’s life (modified versions exist to accommodate dividends).

- Efficient Market: The market is efficient, meaning information is immediately reflected in prices.

- Constant Volatility: Volatility remains constant over the option’s life (a major point of contention in practice).

- Risk-Free Rate is Constant: The risk-free interest rate remains constant over the option’s life.

- Lognormal Distribution: Stock prices follow a lognormal distribution.

- No Transaction Costs or Taxes: These are ignored for simplicity.

The Formula (Simplified Explanation)

The Black-Scholes formula, while complex-looking, essentially calculates the expected value of the option at expiration, discounted back to the present. It involves calculating two intermediate values, d1 and d2, using the inputs mentioned above. These values are then plugged into the cumulative standard normal distribution function (N(x)), which represents the probability that a random variable from a standard normal distribution will be less than x.

For a call option, the formula is roughly:

Call Option Price = S * N(d1) – K * e^(-rT) * N(d2)

Where e is the base of the natural logarithm.

Limitations and Practical Use

Despite its widespread use, the Black-Scholes model has limitations. The assumption of constant volatility is particularly problematic, as volatility tends to fluctuate in reality. Furthermore, the model doesn’t perfectly account for “fat tails” in stock price distributions (extreme price movements happen more frequently than a normal distribution would predict). The difficulty in accurately estimating future volatility is a major challenge.

In practice, the Black-Scholes model serves as a benchmark. Traders often use it to identify potentially mispriced options and to manage risk, particularly when hedging option positions. Implied volatility, derived by plugging the market price of an option back into the Black-Scholes formula, provides a valuable measure of market expectations for future price fluctuations.

1000×724 black scholes finance lawscom from finance.laws.com

1000×724 black scholes finance lawscom from finance.laws.com  1600×1024 black scholes excel pricing model eloquens from www.eloquens.com

1600×1024 black scholes excel pricing model eloquens from www.eloquens.com  1920×951 black scholes option pricing excel model add privately from www.eloquens.com

1920×951 black scholes option pricing excel model add privately from www.eloquens.com  720×540 finance black scholes model from present5.com

720×540 finance black scholes model from present5.com  1282×569 steps black scholes model magnimetrics from magnimetrics.com

1282×569 steps black scholes model magnimetrics from magnimetrics.com  1920×1417 option excel model black scholes formula eloquens from www.eloquens.com

1920×1417 option excel model black scholes formula eloquens from www.eloquens.com