Operating cash flow (OCF) is a crucial financial metric reflecting a company’s ability to generate cash from its core business activities. It essentially measures the cash coming in and out as a direct result of selling goods or services, distinct from cash flows related to investments or financing.

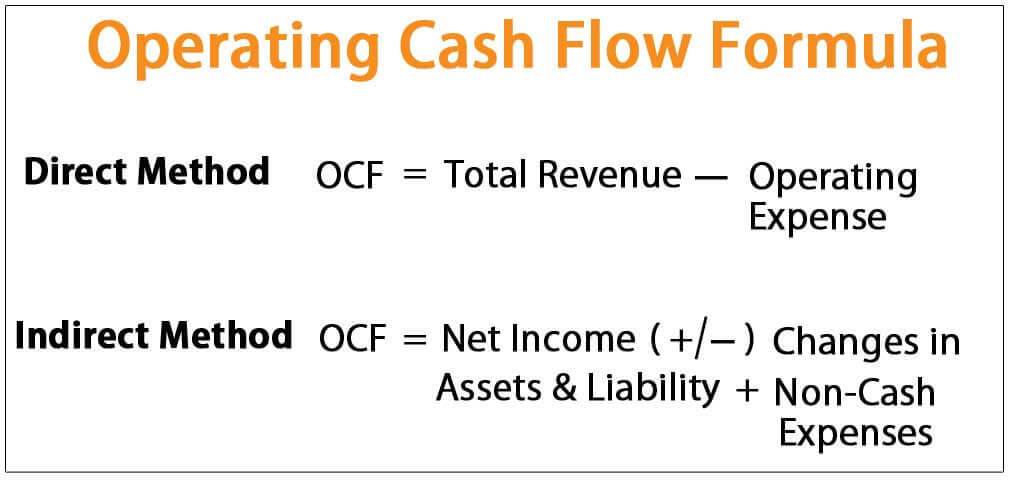

Calculating OCF is typically done using two methods: the direct and indirect methods. The direct method sums up all cash inflows from customers and subtracts all cash outflows for operating expenses like salaries, rent, and inventory. While conceptually straightforward, it’s rarely used due to the difficulty of tracking every cash transaction directly. Instead, companies favor the indirect method.

The indirect method starts with net income, found on the income statement, and then adjusts it for non-cash items and changes in working capital accounts. Common adjustments include:

*

Adding back non-cash expenses: Depreciation and amortization are significant. These represent the allocation of the cost of assets over time, but they don’t involve actual cash outlays in the current period. Similarly, deferred taxes, which arise from temporary differences between taxable income and accounting income, are added back.

*

Adjusting for changes in current assets and liabilities: These adjustments reflect the impact of working capital management on cash flow. An increase in accounts receivable, for example, means the company has made sales but hasn’t collected the cash yet, so it’s subtracted from net income. Conversely, a decrease in accounts receivable means the company collected more cash than it recorded in sales, so it’s added. An increase in accounts payable (delaying payment to suppliers) increases cash flow, while a decrease decreases cash flow. Similar adjustments are made for inventory, prepaid expenses, and accrued liabilities.

Understanding OCF is vital for several reasons. It provides a clear picture of a company’s fundamental earning power. A healthy and consistently positive OCF indicates a company can fund its operations, pay its debts, invest in growth, and distribute dividends without relying solely on external financing. Conversely, a consistently negative OCF signals potential financial distress, suggesting the company may be struggling to generate enough cash from its core business to cover its expenses.

Furthermore, OCF is used in various financial analyses and valuation models. Free cash flow (FCF), a key metric for valuing companies, is derived from OCF by subtracting capital expenditures (the cost of purchasing or upgrading fixed assets). Analysts also use OCF to assess a company’s liquidity and solvency, as it provides insights into its ability to meet its short-term obligations. OCF is also compared to other financial metrics like net income, sales, and capital expenditures to identify trends and potential red flags.

In summary, operating cash flow is a critical indicator of a company’s financial health and its ability to generate cash from its day-to-day operations. Analyzing OCF and understanding its drivers provides valuable insights for investors, creditors, and management alike.

800×693 operating cash flow basics smartsheet from www.smartsheet.com

800×693 operating cash flow basics smartsheet from www.smartsheet.com  535×308 manage operating cash flows dummies from www.dummies.com

535×308 manage operating cash flows dummies from www.dummies.com  1019×534 operating cash flow efinancemanagementcom from efinancemanagement.com

1019×534 operating cash flow efinancemanagementcom from efinancemanagement.com  1200×675 operating cash flow trading activities double entry bookkeeping from www.double-entry-bookkeeping.com

1200×675 operating cash flow trading activities double entry bookkeeping from www.double-entry-bookkeeping.com  620×428 operating cash flow ocf definition meaning from www.myaccountingcourse.com

620×428 operating cash flow ocf definition meaning from www.myaccountingcourse.com  1024×485 operating cash flow formula calculation examples from www.wallstreetmojo.com

1024×485 operating cash flow formula calculation examples from www.wallstreetmojo.com /cash-flow-concept-992325826-02e39ab9d9394062817a6dd4c62b7a56.jpg) 5616×3744 operating cash flow ocf definition from www.investopedia.com

5616×3744 operating cash flow ocf definition from www.investopedia.com