Weighted Average Life (WAL) in Finance

Weighted Average Life (WAL) is a crucial metric in finance, primarily used to understand the time it takes for a debt instrument, like a loan or bond, to be repaid. It represents the average time each dollar of principal remains outstanding. Unlike maturity date, which only indicates the final repayment, WAL provides a more accurate picture of the repayment pattern, accounting for principal payments made over the life of the loan or bond.

Understanding the Calculation

The calculation of WAL involves weighting each principal repayment by the time elapsed until that repayment occurs. Here’s the breakdown:

- Determine the Principal Repayment Schedule: This involves identifying the amount of principal repaid in each period (e.g., annually, quarterly, monthly).

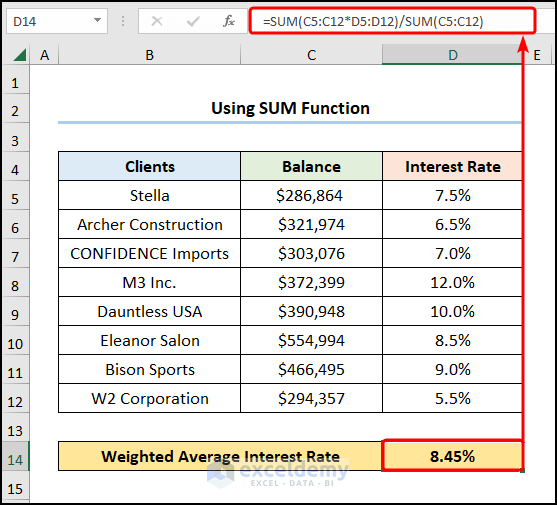

- Calculate the Proportion of Principal Repaid in Each Period: Divide the principal repaid in each period by the total initial principal amount. This gives you the weight for each period.

- Multiply the Weight by the Time Period: Multiply the proportion of principal repaid in each period by the time (in years or fractions of years) from the initial date until that repayment.

- Sum the Results: Add up the results from step 3 for all periods. The final sum is the weighted average life.

The formula can be expressed as:

WAL = Σ (t * (Pt / P))

Where:

- WAL = Weighted Average Life

- t = Time until principal payment (in years)

- Pt = Principal payment at time t

- P = Total initial principal amount

Importance and Applications

WAL is important for several reasons:

- Risk Assessment: A longer WAL generally indicates higher risk. This is because the investor’s capital is tied up for a longer period, making them more vulnerable to changes in interest rates and other market conditions.

- Duration Calculation: WAL is closely related to duration, a measure of a bond’s sensitivity to interest rate changes. While WAL isn’t a direct substitute for duration (especially for complex securities), it provides a useful estimate.

- Portfolio Management: WAL helps portfolio managers understand the overall maturity profile of their debt holdings and manage interest rate risk accordingly. By knowing the WAL of their assets and liabilities, they can better match their maturities and reduce the potential for losses.

- Comparison of Investments: WAL allows for a more accurate comparison of different debt instruments. A bond with a shorter maturity but substantial deferred principal payments might have a longer WAL than a bond with a longer maturity but significant early principal repayments.

- Prepayment Modeling: For mortgage-backed securities (MBS) and other amortizing assets, WAL is particularly useful because it is sensitive to changes in prepayment rates. Faster prepayments will shorten the WAL, while slower prepayments will lengthen it.

Limitations

While WAL is a valuable tool, it has limitations. It assumes a constant discount rate and doesn’t fully capture the complexities of interest rate sensitivity. Duration is a more comprehensive measure of interest rate risk. Furthermore, WAL doesn’t account for embedded options, such as call provisions, which can significantly impact the actual life of a bond. Prepayment risk in mortgages can also make estimating WAL difficult, requiring sophisticated modeling.

In conclusion, the weighted average life provides a useful and easily understandable metric for estimating the average time it takes to receive principal repayments on a debt instrument, enabling better risk assessment and portfolio management.

709×575 weighted average loan life finexmod from www.finexmod.com

709×575 weighted average loan life finexmod from www.finexmod.com  699×93 weighted average life wal quick guide dcf exchange from www.dcfexchange.com

699×93 weighted average life wal quick guide dcf exchange from www.dcfexchange.com  1280×675 weighted average life wal awesomefintech blog from www.awesomefintech.com

1280×675 weighted average life wal awesomefintech blog from www.awesomefintech.com  1024×526 weighted average formula calculator excel template from www.educba.com

1024×526 weighted average formula calculator excel template from www.educba.com :max_bytes(150000):strip_icc()/WeightedAverage-7f9d2614543a4e758e7c8337cfbe6430.jpeg) 1500×1000 weighted average life from www.thebalancemoney.com

1500×1000 weighted average life from www.thebalancemoney.com  640×426 calculate weighted average life bonds sapling from www.sapling.com

640×426 calculate weighted average life bonds sapling from www.sapling.com  1472×779 weighted average life andi support center from support.andi.com

1472×779 weighted average life andi support center from support.andi.com  350×350 weighted average examples from www.someka.net

350×350 weighted average examples from www.someka.net :max_bytes(150000):strip_icc()/weightedaveragelife.asp-final-ec0519049cb84754844f37b0fb7ef5e9.png) 1500×1013 understanding weighted average life wal works from www.investopedia.com

1500×1013 understanding weighted average life wal works from www.investopedia.com  1024×223 solved hy weighted average life wal cheggcom from www.chegg.com

1024×223 solved hy weighted average life wal cheggcom from www.chegg.com  750×243 weighted average maturity wam definition from investinganswers.com

750×243 weighted average maturity wam definition from investinganswers.com  1000×664 weighted average life structured settlement annuities dcf exchange from www.dcfexchange.com

1000×664 weighted average life structured settlement annuities dcf exchange from www.dcfexchange.com  1280×720 weighted average life powerpoint layouts cpb from www.slideteam.net

1280×720 weighted average life powerpoint layouts cpb from www.slideteam.net  1280×720 weighted average life maturity powerpoint google cpb from www.slideteam.net

1280×720 weighted average life maturity powerpoint google cpb from www.slideteam.net  567×403 weighted average maturity weighted average life from hangestijumong.blogspot.com

567×403 weighted average maturity weighted average life from hangestijumong.blogspot.com  1657×564 weighted average supermoney from www.supermoney.com

1657×564 weighted average supermoney from www.supermoney.com  1344×576 weighted average life bond calculation excel design talk from design.udlvirtual.edu.pe

1344×576 weighted average life bond calculation excel design talk from design.udlvirtual.edu.pe  3000×2250 weighted average cost capital wacc cheat sheet eloquens from www.eloquens.com

3000×2250 weighted average cost capital wacc cheat sheet eloquens from www.eloquens.com  1024×458 solved weighted average cost capital personal finance cheggcom from www.chegg.com

1024×458 solved weighted average cost capital personal finance cheggcom from www.chegg.com  850×691 external finance weighted average leverage firm invests from www.researchgate.net

850×691 external finance weighted average leverage firm invests from www.researchgate.net  875×909 average life definition determination role investment from www.financestrategists.com

875×909 average life definition determination role investment from www.financestrategists.com  557×505 calculate weighted average life excel mandy leon blog from storage.googleapis.com

557×505 calculate weighted average life excel mandy leon blog from storage.googleapis.com  1791×826 formula weighted average life dorothy frost blog from exozflqcl.blob.core.windows.net

1791×826 formula weighted average life dorothy frost blog from exozflqcl.blob.core.windows.net