“`html

Understanding the PMT Finance Formula

The PMT formula is a powerful tool in finance used to calculate the periodic payment amount required to pay off a loan or reach a savings goal. It’s widely utilized in calculating mortgage payments, car loan installments, and retirement savings plans.

At its core, the PMT formula considers several key factors:

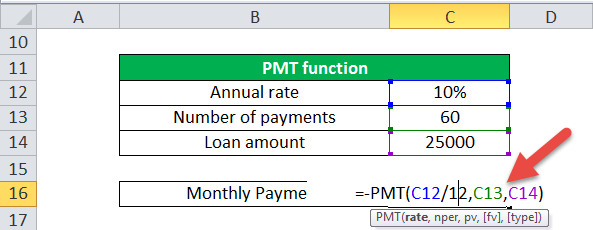

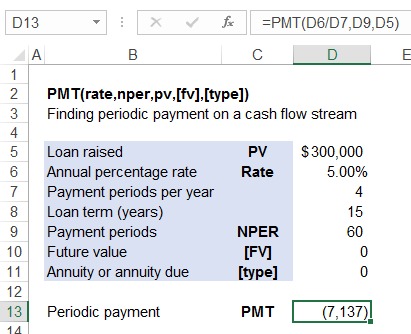

* **Rate (r):** This represents the interest rate per period. Importantly, the annual interest rate needs to be adjusted to match the payment frequency. For example, if the annual interest rate is 6% and payments are made monthly, the rate per period would be 6%/12 = 0.005. * **Nper (n):** This signifies the total number of payment periods. Again, this needs to be consistent with the payment frequency. For a 5-year loan with monthly payments, nper would be 5 * 12 = 60. * **Pv (pv):** This stands for the present value or the principal amount of the loan or investment. For a loan, this is the initial amount borrowed. * **Fv (fv):** This represents the future value. For a loan being paid off, the future value is typically 0. For a savings goal, it’s the desired amount you want to accumulate. If omitted, it’s usually assumed to be 0. * **Type (type):** This indicates when payments are made. If payments are made at the end of the period (ordinary annuity), type is 0 (or omitted). If payments are made at the beginning of the period (annuity due), type is 1.

The PMT formula is expressed as:

PMT = (r * (Pv + Fv/(1 + r)^n)) / (1 – (1 + r)^-n)

This formula might seem intimidating, but it breaks down logically:

* The numerator (r * (Pv + Fv/(1 + r)^n)) calculates the interest earned on the present value plus the discounted future value. Discounting the future value accounts for the time value of money. * The denominator (1 – (1 + r)^-n) represents the present value of an annuity stream of $1 for n periods at rate r.

Financial calculators and spreadsheet software (like Excel or Google Sheets) have built-in PMT functions that simplify the calculation. These functions generally take the same arguments as the formula: RATE, NPER, PV, FV, and TYPE.

It’s crucial to understand that the PMT function returns a negative value when calculating loan payments because it represents an outflow of cash. If you want the payment displayed as a positive number, you can either multiply the result by -1 or enter the present value (Pv) as a negative number.

The PMT formula is a valuable tool for making informed financial decisions. By understanding how it works and what factors influence the payment amount, you can effectively plan for your financial future and manage your debt responsibly.

“`

565×259 pmt function excel calculate payment amounts from www.automateexcel.com

565×259 pmt function excel calculate payment amounts from www.automateexcel.com  553×231 pmt function excel exercise file from spreadsheeto.com

553×231 pmt function excel exercise file from spreadsheeto.com  667×271 pmt function excel formula examples pmt from www.educba.com

667×271 pmt function excel formula examples pmt from www.educba.com  700×400 excel pmt function exceljet from exceljet.net

700×400 excel pmt function exceljet from exceljet.net  593×230 pmt function excel formula examples from www.wallstreetmojo.com

593×230 pmt function excel formula examples from www.wallstreetmojo.com  411×334 excel pmt function calculation from xplaind.com

411×334 excel pmt function calculation from xplaind.com