The Black-Scholes Model: Pricing Options

The Black-Scholes model, developed by Fischer Black and Myron Scholes in 1973, is a mathematical formula used to estimate the theoretical price of European-style options. It’s a cornerstone of modern financial theory and widely used by traders and investors to understand option pricing dynamics.

At its core, the model assumes that the price of the underlying asset (e.g., a stock) follows a log-normal distribution and that markets are efficient. It relies on several key inputs:

- Current Price of the Underlying Asset (S): The present market price of the stock or asset.

- Strike Price (K): The price at which the option holder can buy (call option) or sell (put option) the underlying asset.

- Time to Expiration (T): The remaining time until the option expires, expressed in years.

- Risk-Free Interest Rate (r): The current risk-free interest rate, typically the yield on a government bond with a maturity similar to the option’s expiration.

- Volatility (σ): The expected volatility of the underlying asset’s price, usually expressed as an annualized standard deviation. This is often the most challenging input to estimate.

The model’s equations calculate two key parameters, d1 and d2, which are then used in conjunction with the cumulative standard normal distribution function (N(x)) to determine the theoretical option price.

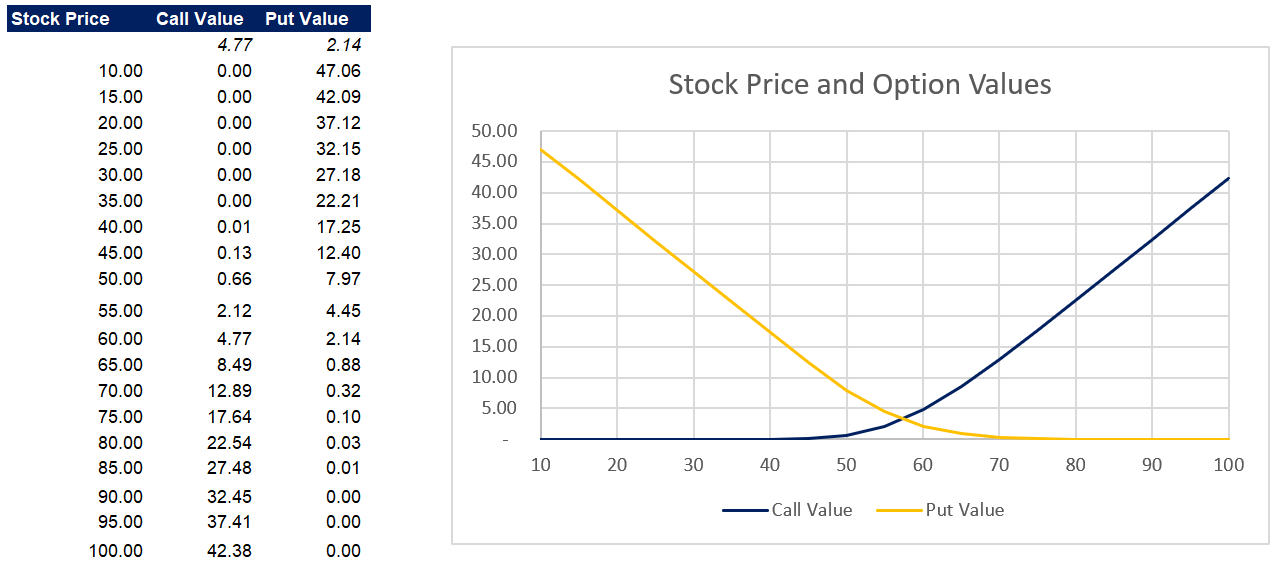

For a Call Option:

C = S * N(d1) – K * e(-rT) * N(d2)

For a Put Option:

P = K * e(-rT) * N(-d2) – S * N(-d1)

Where:

d1 = [ln(S/K) + (r + σ2/2)T] / (σ√T)

d2 = d1 – σ√T

While the Black-Scholes model is valuable, it has limitations. It assumes constant volatility, a risk-free interest rate that remains constant, and that the underlying asset does not pay dividends during the option’s life. It also only applies to European-style options that can only be exercised at expiration. These assumptions rarely hold true in the real world.

Despite these limitations, the Black-Scholes model provides a crucial framework for understanding option pricing and serves as a foundation for more sophisticated models. It allows investors to assess whether an option is overvalued or undervalued, and helps in constructing hedging strategies. The implied volatility derived from the model (by plugging in the market price of the option and solving for volatility) is also a widely used metric to gauge market expectations of future price fluctuations.

1000×724 black scholes finance lawscom from finance.laws.com

1000×724 black scholes finance lawscom from finance.laws.com  1600×1024 black scholes excel pricing model eloquens from www.eloquens.com

1600×1024 black scholes excel pricing model eloquens from www.eloquens.com  1920×951 black scholes option pricing excel model add privately from www.eloquens.com

1920×951 black scholes option pricing excel model add privately from www.eloquens.com  720×540 finance black scholes model from present5.com

720×540 finance black scholes model from present5.com  1282×569 steps black scholes model magnimetrics from magnimetrics.com

1282×569 steps black scholes model magnimetrics from magnimetrics.com  1920×1417 option excel model black scholes formula eloquens from www.eloquens.com

1920×1417 option excel model black scholes formula eloquens from www.eloquens.com